ITAT Ahmedabad Rules: Calculation Error in Section 54F Exemption Not Tax Misreporting

Tribunal Quashes Penalty Against Homebuyer, Says Mistakes Do Not Equal Concealment

Judgment Reinforces Fairness in Tax Compliance and Relief for Genuine Errors

By Our Legal Reporter

New Delhi: November 28, 2025:

In a landmark decision that will resonate with taxpayers across India, the Income Tax Appellate Tribunal (ITAT), Ahmedabad Bench, has ruled that a mere calculation error in claiming exemption under Section 54F of the Income Tax Act, 1961 does not amount to misreporting of income. The tribunal quashed the penalty imposed on a homebuyer, offering significant relief and setting a precedent for similar cases.

Also Read: Karnataka High Court Quashes GST Registration Cancellation Over Lack of Mandatory Hearing

Background of the Case

The case involved Mr. Sanghvi, a taxpayer who sold a long-term asset and invested the proceeds in purchasing a residential property. He claimed exemption under Section 54F, which allows relief from capital gains tax when such reinvestment is made. However, while filing his return, he miscalculated the eligible exemption amount.

The tax authorities treated this miscalculation as furnishing inaccurate particulars of income and imposed a penalty under Section 270A (9) of the Income Tax Act. The penalty was challenged before the ITAT.

Tribunal’s Observations

- The taxpayer had disclosed all relevant facts and documents.

- The error was only in computation, not in concealment of income.

- A mistake in calculating exemption cannot be equated with deliberate misreporting.

The tribunal emphasized that penalties are meant to deter intentional concealment or fraud, not to punish genuine mistakes. Accordingly, the penalty was declared null and void.

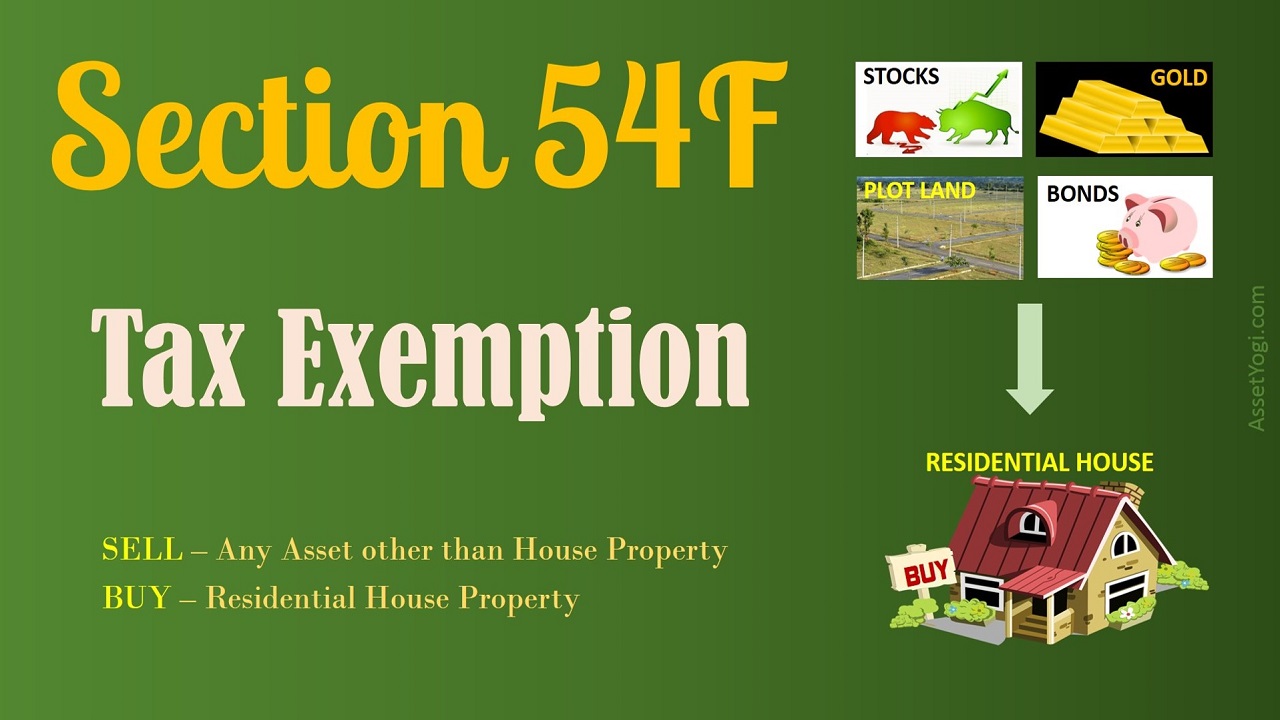

Section 54F Explained

Section 54F provides tax exemption on capital gains if:

- The taxpayer sells a long-term asset other than a residential house.

- The net consideration is invested in purchasing or constructing a residential house within prescribed timelines.

- The exemption is proportionate to the amount invested.

Also Read: Bombay High Court: Crocin Trademark Sale to UK Firm Is Export, Exempt from Maharashtra Sales Tax

For example, if a taxpayer invests the entire sale proceeds in a new house, full exemption is available. If only part is invested, exemption is proportionate. Errors often occur in calculating this proportion, leading to disputes.

Importance of the Ruling

This ruling is significant because:

- Clarifies Law: It distinguishes between genuine errors and deliberate misreporting.

- Protects Taxpayers: Honest taxpayers who disclose all facts but make mistakes will not face harsh penalties.

- Encourages Compliance: By reducing fear of penalties for minor errors, it promotes voluntary compliance.

Similar Cases and Trends

Across India, courts and tribunals have dealt with multiple disputes under Section 54F:

- Moneycontrol Report (2025): ITAT Ahmedabad allowed exemption even when the taxpayer failed to deposit unutilized capital gains in the Capital Gains Account Scheme, provided the money was ultimately invested in a house.

- TaxGuru Case (2009): ITAT Chennai denied exemption for multiple flats, holding that Section 54F permits exemption only for a single residential unit.

- Delhi High Court (2024): Observed that technical lapses should not override substantive rights when taxpayers act in good faith.

These cases show a trend toward judicial leniency in genuine situations while maintaining strictness against misuse.

Also Read: Bombay High Court: Crocin Trademark Sale to UK Firm Is Export, Exempt from Maharashtra Sales Tax

Expert Views

- The decision reinforces the principle of natural justice.

- It provides clarity for taxpayers who often struggle with complex calculations.

- It highlights the importance of full disclosure—errors may be excused, but concealment will not.

Impact on Homebuyers and Investors

- Documentation: Maintain complete records of transactions and investments.

- Transparency: Disclose all facts honestly, even if unsure about calculations.

- Professional Advice: Consult tax experts to avoid errors but know that genuine mistakes are not punishable.

Broader Implications

- Authorities may adopt a more balanced approach, distinguishing between fraud and error.

- Taxpayers may feel more confident in making claims under Section 54F.

- It could reduce litigation, as penalties for minor mistakes may be challenged successfully.

Conclusion

The ITAT Ahmedabad’s decision is a milestone in tax jurisprudence. It sends a clear message: tax law is strict, but fairness must prevail. Mistakes in calculation should not be treated as misreporting, provided taxpayers act in good faith and disclose all facts.

This ruling will not only protect individual taxpayers but also strengthen trust in the tax system. For homebuyers and investors, it is a reminder that while compliance is essential, the law recognizes human error and ensures justice.

📌 Keywords for SEO (Google + ChatGPT)

- ITAT Ahmedabad Section 54F ruling

- Section 54F tax exemption calculation error

- Homebuyer tax penalty relief India

- Income Tax Appellate Tribunal capital gains exemption

- Section 270A penalty misreporting case

- Capital gains exemption under Section 54F

- ITAT ruling on tax misreporting India

- Tax exemption relief for homebuyers

- Section 54F proportionate exemption calculation

- Tax tribunal judgment October 2025